Market risk assessment: A multi-asset, agent-based approach applied to a DeFi lending protocol

Abstract

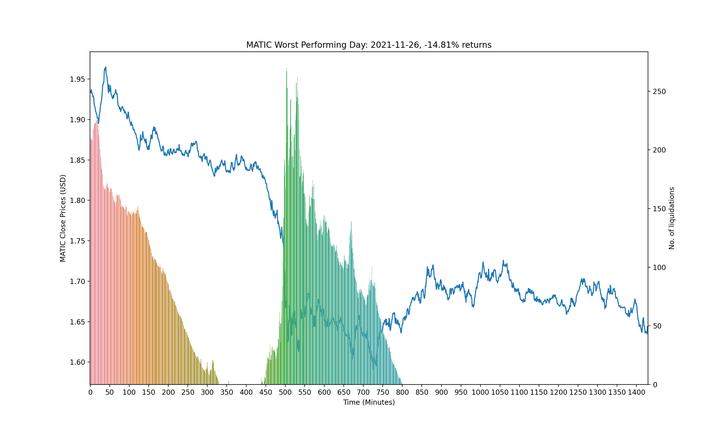

We assess the market risk of the 0VIX lending protocol using a multi-asset agent-based model to simulate ensembles of users subject to price-driven liquidation risk. Our multi-asset methodology shows that the protocol’s systemic risk is small under stress and that enough collateral is always present to underwrite active loans. Our simulations use a wide variety of historical data to model market volatility and run the agent-based simulation to show that even if all the assets like ETH, BTC and MATIC increase their hourly volatility by more than ten times, the protocol carries less than 0.1% default risk given suggested protocol parameter values for liquidation loan-to-value ratio and liquidation incentives.